If you’re a legal services attorney, as I was for many years, you’ve got more pressing client needs than you can meet. Your days are full, and there is always another client waiting. You probably got into the job because you felt a calling, although some days it can be hard to see if you are making a difference. Injustice abounds, and your tools can feel limited. This can be true for all kinds of grassroots organizers, social service providers, and advocates—the world is crying out for change and our time and energy is limited.

And, right now, that cry for change and those pressing client needs are more pressing than ever. COVID-19 has laid bare in the most stark and chilling terms the life-destroying impact that generations of racism, racial inequality, and poverty have had. African Americans, Latinos, and Native Americans are all dying at vastly disproportional rates. We’ve seen violent suppression by the state of legitimate calls to address centuries of oppression. There is a renewed urgency to our collective work for racial and economic justice.

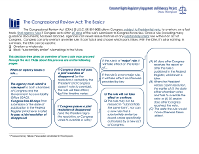

So, why? Why do regulatory advocacy? Rules take forever to get written, and, at the federal level, we are facing an administration bent on removing regulatory protections. The President’s tweets, if not the agencies’ agendas, indicate implacable hostility to fair housing and fair lending, at least as those terms have been commonly understood.

Here’s why. Regulatory advocacy allows us to tap into power. The work of implementing and maintaining legislative victories happens in the regulatory agencies. Regulatory agencies set the rules for who can live in public housing, the terms on which hungry children and their families can get food stamps or public assistance, and who can apply for asylum and how. To take the specific core building blocks of economic justice and access to credit, one agency, the Consumer Financial Protection Bureau controls the rules about how credit reporting is done, what happens when you can’t pay your mortgage or payday loan, and the terms on which that mortgage or payday loan are made, including whether and how a lender can discriminate against you. Regulatory advocacy, quite simply, lets us help set the framework in which all the rest of our work and advocacy for justice and equity takes place.

Regulatory advocacy also leverages what we know and do well. Regulatory agencies are required by law to ask us—all of us—what we think the impacts of their proposed regulations will be and what better approaches to solving the problem exist. Anyone who works representing legal-services clients will know intimately the impact of laws and regulations on their clients and client communities. And that detailed, specific, concrete knowledge is exactly what regulators most often struggle to get and are required to consider—if we give it to them.

And here’s why, too. Remember how I earlier mentioned the racial disparities in death rates from COVID-19? We only know that because a lot of people did a lot of regulatory advocacy. Early on, in the pandemic, demographic data collection was spotty. It wasn’t until June 4 that the U.S. Department of Health and Human Services required reporting of demographic data along with COVID-19 test results. Advocates pressed the government at the county, state, and federal level to collect and release demographic data. And they were successful. Having those numbers out there in the public has changed the narrative and enabled further advocacy to address systemic imbalances.

There are always avenues for regulatory advocacy and always a need for regulatory advocacy. If we don’t do the regulatory advocacy, other people will, and the stories they tell will not be the ones we would tell, and the results they get will not reflect the actual lived experiences of our communities.

In the coming weeks, we’ll be rolling out on this website a range of documents to try to help support your work in regulatory advocacy. We hope you’ll subscribe to receive our work and let us know what works for you and what doesn’t.